From Beyond Public and Private

Submitted by ChrisCook on Monday, 23 February, 2009 – 10:24 Chris Cook

Beyond Public and Private – Chris Cook, 20 February 2009

21st Century problems cannot be fixed by 20th Century solutions”….Dr Narsi Ghorban

The Credit Crash marks the end of an era for the global financial system, and the beginning of another. Few understand our modern banking system, but in simple terms it consists of banks as “credit intermediaries” who create credit based upon an amount of capital specified by international banking regulators.

This interest-bearing credit constitutes most of the money in use, the balance (<3%) being notes and coin. Most people think that banks take in deposits and lend them out again, but a moment’s thought will establish that if that were the case, then there could not be any new money. In fact banks create credit as new money, and this is instantaneously deposited somewhere in the system.

However, it was not Bank capital which underpinned the credit which inflated the massive recent bubbles in Property and Private Equity. It was in fact the capital of investors to whom Banks had “out-sourced” credit risk through securitisation, credit derivatives, credit insurance and toxic “diced and sliced” cocktails of all three – such as “Collateralised Debt Obligations” (CDOs).

In or around mid 2007 the financial claims of this pyramid of credit exceeded the capacity of the productive economy to meet them – at a point I call the point of “Peak Credit”. From this point on, the bubbles started to deflate, as defaults on loans started to literally destroy money.

This process continues to gather pace and governments are now pumping money into Banks in an attempt to stem the destruction of capital and the haemorrhage of credit. But to treat these visible wounds does nothing to stem the massive invisible internal bleeding from the “shadow banking system” of investors. Transfusions of new credit are useless unless this bleeding is stopped. To do so will require surgery, not the further application of leeches.

I believe that credit must be reinvented, and re-based, and that this is possible through a new approach to direct investment in productive assets such as land and renewable energy.

But what do we mean by “investment”? In fact there is no mechanism for investment by the Public sector: it is excluded by the definitions we are accustomed to using.

Governments may either fund assets directly from taxes, or borrow at interest: there is by definition no possibility of “investment” in public assets. Investment may only be “Private”, by which we specifically mean “owned by a Joint Stock Limited Liability Company” – a 19th century legal creation.

While all attention has been on the rapid evolution of the markets in credit, new legal and financial structures, or enterprise models, have quietly been appearing “under the radar screen”. These are based not upon Company law but upon “judge made” Trust law and the consensual law of Partnership.

It is in the imaginative use of partnership frameworks for investment in productive assets that I have identified and developed a legal innovation enabling a solution to the current crisis.

Introducing the Open Corporate

On 6 April 2001 a new UK legal entity, the Limited Liability Partnership (LLP), came into effect in order to protect professional partnerships. Confusingly, an LLP is not legally a partnership. It is, however – like a Corporation – a corporate body with a continuing legal existence independent of its members. Also, as with a limited liability company, you cannot lose more than you invest in an LLP.

The `LLP agreement’ between members is totally flexible and need not even be in writing, since simple provisions based upon partnership law apply by way of default. The LLP may truly be thought of as an “Open” Corporate, and it is being used for purposes never envisaged.

In particular, it is being used as a framework for investment in productive assets of all kinds. LLP’s are routinely in use in the public sector, and the City of Glasgow currently has three municipal LLP joint ventures, albeit conventionally financed.

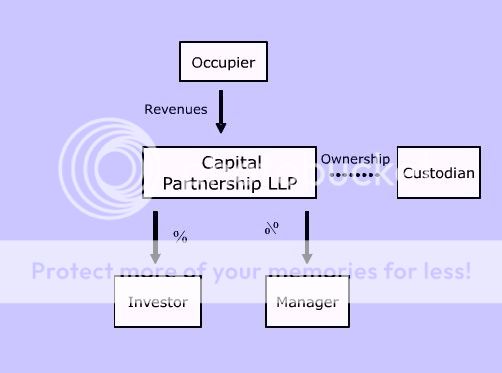

The Hilton Group first demonstrated the potential of an LLP framework for development and long term financing in a > £1bn plus Capital Partnership.

The Capital Partnership allows risk and reward to be shared equitably in proportional shares of production or revenues : in a good year, Hilton and Investors have a good year; and in a bad year, they share the pain.

This model has universal application, and any enterprise; whether Public or Private; commercial, social or even charitable in aims; whatever the legal form; may opt to share production or revenues in this way.

Within a Capital Partnership framework it is possible to create:

(a) Equity Shares – proportional shares which are not redeemable (there must always be 100%) but may be transferable.

(b) Units – redeemable in “money’s worth” such as Kilo Watt Hours;

and these enable entirely new mechanisms for the financing of assets of all kinds.

In particular, we may create a new class of Community-owned enterprises which allow the production or revenues from assets in Public ownership to be shared equitably as between the providers and users of finance. Let’s have a look at how this might work.

Community Energy Partnership – Energy and Heat Pools

Imagine that a community wishes to finance a wind turbine. The turbine is held by a custodian, and Units are created redeemable for (say) 10 Kilo Watt Hours of energy each, which are then sold to investors. The sale of between 30 and 40 percent of production will typically finance a turbine. After a percentage of production is allocated to a manager, the balance from the Energy Pool will be an “Energy Dividend” to the Community.

Investment in energy savings is also possible through (say) retrofitting Combined Heat and Power. Investment by a local “Heat Pool” fund will finance the CHP connection of the houses. It results in an “Energy Loan” denominated in energy, to the house, not the owner. This energy-denominated investment is then repaid to the Heat Pool at the market price of energy. The savings in energy value are therefore shared between the property occupier and the investors.

Community Land Partnership – Rental Pools

Imagine that a bank has a portfolio of “distressed” properties which are about to be repossessed.

These properties may instead be transferred to a custodian, such as a local municipality, and a rental may be set at an affordable level which is then index-linked. The resulting Rental Pool is then divided into proportional units (eg billionths) allocated between Investors and a Manager.

For occupiers, this is a new form of rent-to-buy, since any amount paid in excess of the rental will enable them to buy Units. For investors, Units provide a reasonable, index-linked, secure revenue stream, ideal for risk averse long term investors such as pension funds.

For Banks with a portfolio of distressed mortgage loans this “asset-based” form of refinancing will raise more money than any debt-based refinancing which leaves intact the obligation to repay the loan.

While the Community Land Partnership opens up a way of refinancing existing property, it also opens up new options for the sustainable development of new property. If the model is used for new development it is in the interests of a Developer member to develop to high standards of quality and energy efficiency since this will minimise the cost of occupation and therefore maximise the rental value. The Developer’s interests are therefore aligned with those of everyone else.

Outcomes

These partnerships require no legislation, since they are based upon consensual agreements that individuals and enterprises are free to enter, or not, at their discretion. This proposal therefore complements and augments the existing system: it is not an alternative to it.

Through omitting a repayment date, credit evolves into an open-ended form of Equity. A new generation of direct “Peer to Peer” investment in Units of production or revenues from productive assets may evolve to complement conventional secured debt and shares in companies.

A partnership-based model enables new possibilities for direct investment in “Community Equity”and even “Municipal Equity” which together constitute a “National Equity”.

Why sell ownership and control of assets when it is possible to unitise production or revenues and sell it to stakeholders?

In this networked “Peer to Peer” model, banks need no longer act as credit intermediaries putting capital at risk by creating credit based upon it. They may instead become providers of investment banking services, and managers of bilateral “trade” credit creation.

By addressing the Quality of credit, rather than its Quantity we may address the Credit Crash and avoid both the conventional unpleasant economic choices of Depression – caused by a drastic reduction in the quantity of credit; and Inflation – caused by increasing the quantity of credit in order to avoid Depression.

So, to conclude, in the networked 21st Century economy we may transcend conventional alternatives and go beyond Public and Private.

A friend of mine just emailed me one of your articles from a while back. I read that one a few more. Really enjoy your blog. Thanks

Hello. I was reading someone elses blog and saw you on their blogroll. Would you be interested in exchanging blog roll links? If so, feel free to email me.

Thanks.

[…] article at http://tx1.fcomet.com/~claverto/cms/beyond-public-and-private-chris-cook.html […]